516-301-0328

LLC vs. S Corp: Which Structure Saves You More on Taxes?

Blog post description.

5/30/20263 min read

LLC vs Scorp

LLC vs. S Corp: Which Structure Saves You More on Taxes?

If your business is making money and you haven't looked at your entity structure lately, there's a good chance you're overpaying the IRS — not by a little, either. We're talking thousands of dollars a year in taxes you didn't need to pay.

A lot of business owners assume having an LLC is the strategy. It's not. The real strategy is knowing when to make the S corporation election.

The biggest misconception about LLCs

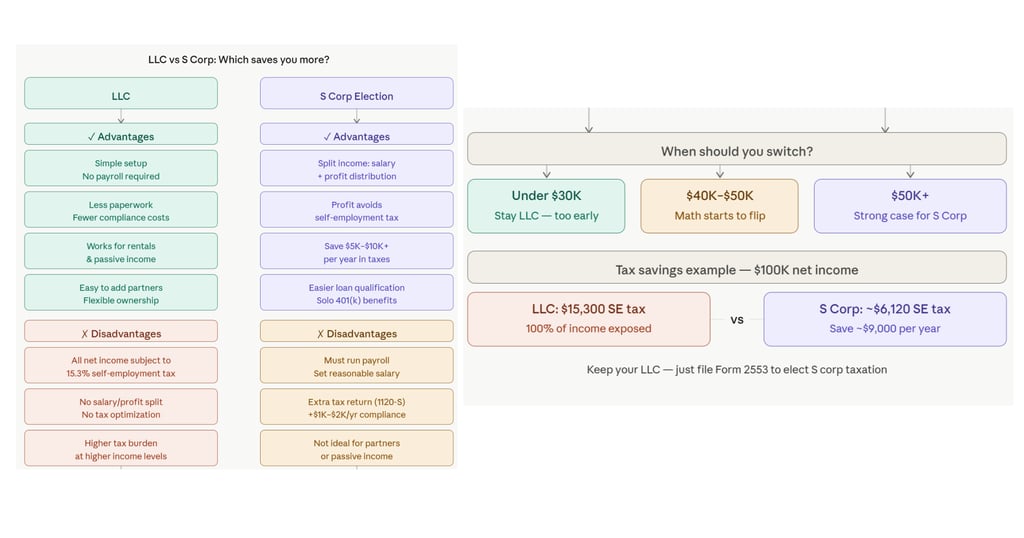

An LLC doesn't save you taxes by itself. It gives you liability protection — which is important — but from a tax standpoint, it's usually treated as a sole proprietorship or partnership. That means every dollar of net income flows through to your personal return and gets hit with self-employment tax.

That tax is 15.3%, and it applies before you even start calculating income tax. Think of it as your automatic tip to the IRS. This is exactly where most business owners lose money without realizing it, and why the S corp conversation matters so much.

What an S Corp does differently

An S corporation isn't a new entity you have to create. You keep your LLC and simply elect to have it taxed differently. That one change allows you to split your income into two categories: a reasonable salary and remaining profit. The salary portion is subject to payroll taxes — but the remaining profit is not. That shift is where the savings happen.

Where the tax savings happen

Here's a simple example. If your business nets $100,000 as a standard LLC, the entire amount is subject to self-employment tax — over $15,000 to the IRS before income tax enters the picture.

Run that same $100,000 through an S corp structure: you pay yourself a reasonable salary of $40,000, and the remaining $60,000 comes through as profit. Only the $40,000 is subject to payroll taxes. The $60,000 avoids that 15.3% hit entirely. That's roughly $9,000 in savings in a single year — and that benefit repeats every year.

When should you switch?

Timing is everything here. Switch too early and the savings won't outweigh the added costs. Wait too long and you leave money on the table every year.

Under $30K net: too early — stay LLC

$40K–$50K net: the math starts to flip in your favor

$50K+: the case for S corp becomes very strong

The numbers will tell you when it's time. You don't have to guess.

How to make the switch

It's simpler than most people think. You're not forming a new business. You keep your existing LLC and file Form 2553 with the IRS to elect S corp status. Think of it as upgrading the operating system inside your business, not rebuilding it from scratch.

Timing does matter — there are deadlines for making the election, and in some cases you may be able to apply it retroactively. Getting this right ensures you don't miss savings you could have captured earlier in the year.

The tradeoffs (and why they're worth it)

An S corp comes with a few additional responsibilities: running payroll, filing an extra tax return (Form 1120-S), and staying compliant with IRS guidelines around reasonable compensation. The added work typically costs $1,000–$2,000 per year in compliance. But if you're saving $5,000, $7,000, or even $10,000 in taxes, the math is obvious.

Bonus benefits

Beyond tax savings, an S corp can open doors to stronger retirement strategies like a Solo 401(k), make it easier to qualify for loans through a clean W-2 salary, and reduce audit risk through more consistent, organized reporting.

Common mistakes to avoid

Switching too early when profits are still low

Setting your reasonable salary too high — eliminating the savings

Putting rental properties or passive investments inside the S corp

Adding family members to payroll without a plan

Waiting too long and missing years of potential savings

The last one is the most expensive mistake. Business owners stay in LLC mode for years without ever revisiting the decision.

The bottom line

This is one of the most important tax decisions you'll make as a business owner. Get it right, and you keep more of what you earn. Ignore it, and you could be overpaying the IRS year after year.

If your business is growing and you're not sure whether it's time to make the switch, book a free 15-minute discovery call to get started. Don't wait until next year — the longer you delay, the more it costs you.